The Chokepoint Guide to Critical Minerals, Part 1: The Foundation

The supply chain running underneath everything. Start here.

There’s a question worth asking the next time you pick up your phone, start your car, or flip on a light switch.

Where did this come from?

Not the device itself. Not the factory that assembled it. But the materials inside it - the ones that make it work at all. Because behind every smartphone, every electric vehicle, every AI server, every precision-guided missile, and every wind turbine is a basket of minerals that most people have never heard of. And almost all of them come from the same place.

That’s what this series is about.

As this post goes live, Donald Trump is in Beijing for what analysts are calling the most consequential U.S.-China summit in a generation. Critical minerals and rare earths are explicitly on the agenda - not as background issues, but as active leverage. China threatened to restrict rare earth flows in April and October 2025. Trump folded both times. Rare earth magnet exports to the US fell 93% year-on-year in May 2025. Even the current truce hasn't fixed the problem - export volumes remain roughly 50% below pre-restriction levels. And a second wave of controls, suspended until November 2026, expires in six months. Even if a deal is announced today, the structural dependency doesn't disappear with a handshake. That context is worth keeping in mind as you read what follows.

What Makes a Mineral “Critical”

The word critical gets used loosely. In this context it has a specific meaning.

A critical mineral is one that meets two conditions simultaneously. First, it’s essential - there’s no practical substitute for it in the application that matters. Second, its supply is concentrated or vulnerable enough that a disruption would cause serious economic or national security damage.

Think of it this way. Iron is essential but not critical - it’s abundant, geographically dispersed, and easy to process. Neodymium - a rare earth element used in the permanent magnets inside every EV motor, every wind turbine generator, and every hard drive - is both essential and concentrated. There is no commercially viable substitute for neodymium in high-performance permanent magnets. And China controls approximately 87% of global rare earth processing.

That combination - irreplaceable and concentrated - is what makes a mineral critical. And the list is longer than most people realize.

The U.S. Geological Survey designates 50 minerals as critical. The European Union lists 34. They include lithium, cobalt, nickel, graphite, copper, rare earth elements, tungsten, gallium, germanium, indium, tellurium, and uranium - among others. Each one is embedded in technologies the modern economy depends on. Each one has a supply chain that most investors have never examined.

The Processing Problem

Here’s where the story gets more complicated - and more important.

Mining and processing are two different things. A country can have significant mineral deposits in the ground and still be completely dependent on another country to turn those deposits into usable material. That’s because processing - the industrial step that converts raw ore into battery-grade lithium, or rare earth concentrate into the purified oxides that go into magnets - requires specialized facilities, technical expertise, and years of investment to build.

China understood this before anyone else did. Over the past two decades, while Western nations focused on the mining layer, China systematically built dominance in the processing layer. The result: even minerals mined outside China often travel to China to be refined before they can be used.

The numbers tell the story plainly.

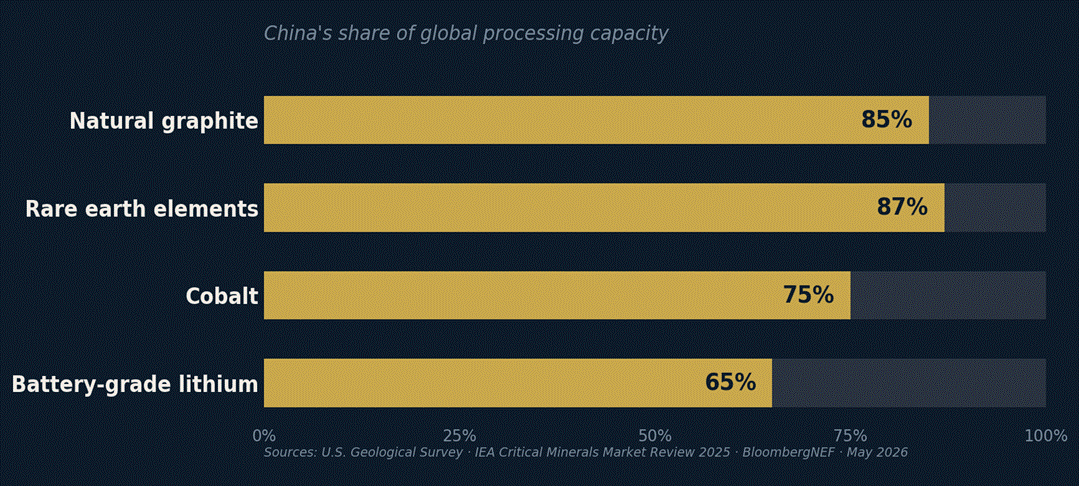

China’s share of global processing capacity across key critical minerals

Lithium is mined primarily in Australia, Chile, and Argentina. But China processes approximately 65% of the world’s battery-grade lithium. Cobalt is mined primarily in the Democratic Republic of Congo. China processes approximately 75% of it. Rare earth elements - mined in China, the United States, and Australia - are processed in China at approximately 87% concentration. Natural graphite, the primary material in EV battery anodes, is processed in China at over 85% concentration. China has had export licensing on graphite since October 2023.

This is not a coincidence. It is the result of deliberate, decades-long strategic investment. And it means that even as Western nations scramble to develop domestic mineral deposits, the ore still needs to go somewhere to be processed. Building alternative processing capacity takes five to ten years of capital-intensive construction - even with full political will and financing in place.

You can’t mine your way out of a processing dependency overnight.

Why This Matters Now More Than Ever

The timing of this supply chain vulnerability couldn’t be worse - or more important to understand.

Three of the most powerful demand forces in the global economy are accelerating simultaneously, and all three require critical minerals as physical inputs.

The AI infrastructure buildout - the data centers, the servers, the cooling systems, the networking equipment - requires rare earth permanent magnets, copper, and specialty metals at a scale that is only beginning to be understood. The $700 billion in AI infrastructure spending committed by the five largest technology companies in 2026 alone is a mineral demand shock that hasn’t been fully priced into supply chain planning.

The energy transition - electric vehicles, grid-scale battery storage, wind turbines, solar panels - requires lithium, cobalt, nickel, graphite, and rare earth elements at a scale that grows every year. Global EV sales reached 17 million units in 2025 and are projected at 40 million by 2030. Each vehicle requires approximately 8-10 kilograms of lithium carbonate equivalent, 10-15 kilograms of nickel, and 5-10 kilograms of cobalt. That’s before grid storage.

Defense modernization - precision-guided munitions, hypersonic missiles, radar systems, military drones, armored vehicles - requires tungsten, rare earths, beryllium, and specialty alloys that have no civilian substitutes and no geopolitical workarounds. Every artillery shell fired in an active conflict is a tungsten consumption event. Every drone requires rare earth magnets in its motors.

Three demand forces. One concentrated supply chain. That’s the structural setup.

The Export Control Era

What was once a theoretical vulnerability is now an active one.

China has begun using its processing dominance as a geopolitical lever. In October 2023, China introduced export licensing requirements for natural graphite - the first direct weaponization of a critical mineral chokepoint. In April 2025, China imposed export controls on seven heavy rare earth elements including dysprosium and terbium - the specific materials needed for high-temperature EV motor performance and defense applications. In May 2026, China halted sulphuric acid exports - a move that cascades through fertilizer production and into global food supply chains in ways most people are only beginning to understand.

Each restriction follows the same pattern: announce, restrict, watch the West scramble. The leverage is real because the alternatives don’t exist yet. Processing infrastructure takes years to build. Supply chains take years to diversify. In the meantime, the dependency persists.

That leverage is sitting at the table in Beijing this week.

This is not a future risk. It is an active, ongoing supply chain reality that is reshaping industrial policy, defense procurement, and investment flows across the developed world.

What Comes Next

This is the first post in a three-part series on critical minerals.

In the next post, we’ll map exactly how specific minerals connect to the technologies and sectors you already know - space, defense, semiconductors, batteries, nuclear, agriculture. The dependency is deeper and more specific than most people realize, and understanding it changes how you see everything from the rockets we covered in our last post to the defense systems, semiconductors, and energy infrastructure that power the modern world.

In Part 2, we’ll look at the investment landscape - the companies across mining, processing, and downstream that are positioned to benefit as the Western world scrambles to build alternative supply chains, and the risks that come with each.

The critical minerals story is the connective tissue running underneath everything else. Once you see it, you can’t unsee it.

The foundation is the import reliance. The dependency map is where it gets specific:

The Chokepoint Guide to Critical Minerals, Part 2: The Dependency Map

In Part 1, we established the foundation: what makes a mineral critical, why the processing layer is the real chokepoint, and how China built its dominance not through geological luck but through decades of deliberate industrial strategy.

This post is for informational purposes only and is not investment advice. The Chokepoint is an independent investment research publication. Nothing in this publication should be construed as a recommendation to buy, sell, or hold any security. All company references and price data are provided for informational and contextual purposes only. Conduct independent due diligence and consult a qualified financial advisor before making any investment decisions.

Financial data sourced from the U.S. Geological Survey, IEA Critical Minerals Market Review 2025, S&P Global Commodity Insights, BloombergNEF, and public market data as of May 2026.

The full archive is at williamdavid.substack.com

Great read! Question for you… Is the primary geopolitical risk actually the location of the rocks in the ground, or is it the chemical processing infrastructure? If we solve the mining side but fail to build high-emissions processing plants at home, have we actually removed the chokepoint?